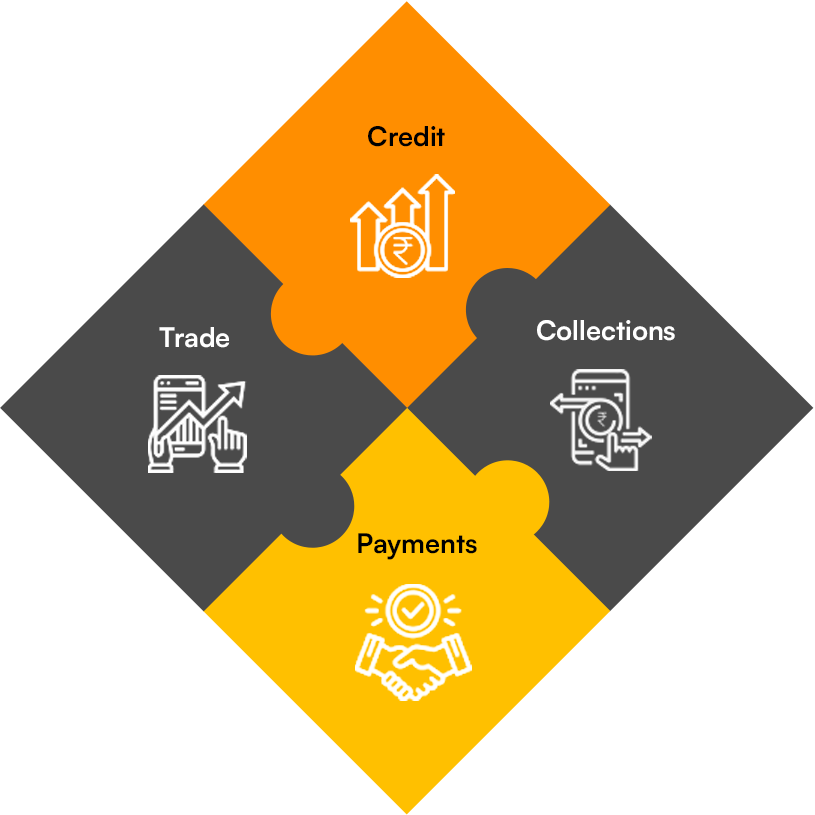

Enterprise Programs

Providing liquidity programs for enterprise eco-systems using state-of-the-art technology platforms.

Financial Institutions

API based Working Capital platform and embedded credit solutions for Financial Institutions and their Customers.

SMEs

Providing an all-in-one credit, trade and cash management platform for small businesses to manage and grow their business.

Nirav Choksi

Co-Founder and CEO

Ram Kewalramani

Co-Founder and MD

Ashutosh Taparia

MD & CRO, Corporate Coverage

Satyam Agrawal

MD, International Business

Manu Prakash

MD and Head – Partnerships & FI Coverage

Debashree Lad

Chief People Officer and Head of Corp. Com

Kapil Kapoor

Chief Product & Technology Officer

Ranjit Singh

Executive Vice President & Head of Credit

Ketan Mehta

Chief Financial Officer

Gaurav Dugar

EVP & General Counsel

The technological waves of disruption have dramatically altered how financial services companies create value for

To thrive in the emerging supply chain ecosystem, it’s time we rethink the traditional value

Effective working capital management is paramount for SMEs in order to maintain their financial stability

As of October 2023, India boasts 111 unicorns—with a combined valuation of $349.67 billion. Last

Global disruptions have highlighted the need for robust and agile supply chains, however, as borrowing

Today, semiconductors are powering trillions of dollars of goods and processes. Poised for a decade

![]()